Simple/Compounded Returns & Drawdowns TableVery excited to bring this script to the public. This is a very useful table that displays the performance of any strategy you give it in a more detailed view. It runs on all timeframes and at any position on the chart with the replay function. It also updates on tick changes. The table consists of three modes: Simple Equity, Compound Equity and Drawdown.

Simple Equity – shows the change in equity for every month and year. It is calculated by finding the difference in initial equity at the beginning of the month/year and the end of the month/year. The table will thus display strategy performance in blocks of time that are not correlated. It is an excellent way to see individual month/year performance from start to finish but it may not represent true change in equity over time. For example, let's assume that 100% of equity is used on every trade for simplicity. If a loss of 50% is made in the first month and a profit of 100% is made in the next month, the strategy will show 50% profit for the year. This aggregate value might be helpful to know for testing purposes, but in reality, the account is actually at break-even for the year (Initial Equity * 0.5 * 2 = Initial Equity).

Compound Equity – shows compounded change in equity for every month and year. It is calculated by finding the difference in starting equity when the strategy is run and equity at the end of the month/year. The table will thus display the true strategy performance – compounded equity at the end of each month/year.

Drawdown – shows max drawdown for every month and year. It is calculated by finding the difference between the highest equity achieved for the month/year and the trough in equity for the same month/year. Notice: strategy tester might have a max drawdown value higher than any of the drawdown values in the table. This is because the strategy tester calculates the difference between the highest and lowest equity for the entire strategy, whereas the table displays drawdowns for months and years only. Sometimes, the max drawdown for the year will also be the max drawdown for the entire strategy; hence the two values will be the same.

To use this table with your own strategy, simply find " PLACE YOUR STRATEGY CODE HERE " at the bottom of the script and place your strategy code there. Special thanks to QuantNomad for the inspiration. As always, please let me know if there are any bugs or if you need some help. Leave a like if you wish!

Cari skrip untuk "STRATEGY TESTER"

Arch1tect's New ToyDescription:

Arch1tect's New Toy tries to predict market trends by simply utilising 2 moving averages crossovers.

How it works:

Buy signals are triggered when the faster MA crosses over the slower MA from the downside to the upside.

Sell signals are triggered when the faster MA crosses under the slower MA from the upside to the downside.

How to use:

Take buys when buy signal is triggered AND close existing sell position

Take sells when sell signal is triggered AND close existing buy position

Note:

Settings are optimised for XAUUSD on the M1 chart.

Extra:

Alerts are included.

You can toggle between EMA , WMA and SMA to your liking.

Strategy Tester version:

EMA Crossover Strategy with Take Profit and Candle HighlightingStrategy Overview:

This strategy is based on the Exponential Moving Averages (EMA), specifically the EMA 20 and EMA 50. It takes advantage of EMA crossovers to identify potential trend reversals and uses multiple take-profit levels and a stop-loss for risk management.

Key Components:

EMA Crossover Signals:

Buy Signal (Uptrend): A buy signal is generated when the EMA 20 crosses above the EMA 50, signaling the start of a potential uptrend.

Sell Signal (Downtrend): A sell signal is generated when the EMA 20 crosses below the EMA 50, signaling the start of a potential downtrend.

Take Profit Levels:

Once a buy or sell signal is triggered, the strategy calculates multiple take-profit levels based on the range of the previous candle. The user can define multipliers for each take-profit level.

Take Profit 1 (TP1): 50% of the previous candle's range above or below the entry price.

Take Profit 2 (TP2): 100% of the previous candle's range above or below the entry price.

Take Profit 3 (TP3): 150% of the previous candle's range above or below the entry price.

Take Profit 4 (TP4): 200% of the previous candle's range above or below the entry price.

These levels are adjusted dynamically based on the previous candle's high and low, so they adapt to changing market conditions.

Stop Loss:

A stop-loss is set to manage risk. The default stop-loss is 3% from the entry price, but this can be adjusted in the settings. The stop-loss is triggered if the price moves against the position by this amount.

Trend Direction Highlighting:

The strategy highlights the bars (candles) with colors:

Green bars indicate an uptrend (when EMA 20 crosses above EMA 50).

Red bars indicate a downtrend (when EMA 20 crosses below EMA 50).

These visual cues help users easily identify the market direction.

Strategy Entries and Exits:

Entries: The strategy enters a long (buy) position when the EMA 20 crosses above the EMA 50 and a short (sell) position when the EMA 20 crosses below the EMA 50.

Exits: The strategy exits the positions at any of the defined take-profit levels or the stop-loss. Multiple exit levels provide opportunities to take profit progressively as the price moves in the favorable direction.

Entry and Exit Conditions in Detail:

Buy Entry Condition (Uptrend):

A buy position is opened when EMA 20 crosses above EMA 50, signaling the start of an uptrend.

The strategy calculates take-profit levels above the entry price based on the previous bar's range (high-low) and the multipliers for TP1, TP2, TP3, and TP4.

Sell Entry Condition (Downtrend):

A sell position is opened when EMA 20 crosses below EMA 50, signaling the start of a downtrend.

The strategy calculates take-profit levels below the entry price, similarly based on the previous bar's range.

Exit Conditions:

Take Profit: The strategy attempts to exit the position at one of the take-profit levels (TP1, TP2, TP3, or TP4). If the price reaches any of these levels, the position is closed.

Stop Loss: The strategy also has a stop-loss set at a default value (3% below the entry for long trades, and 3% above for short trades). The stop-loss helps to protect the position from significant losses.

Backtesting and Performance Metrics:

The strategy can be backtested using TradingView's Strategy Tester. The results will show how the strategy would have performed historically, including key metrics like:

Net Profit

Max Drawdown

Win Rate

Profit Factor

Average Trade Duration

These performance metrics can help users assess the strategy's effectiveness over historical periods and optimize the input parameters (e.g., multipliers, stop-loss level).

Customization:

The strategy allows for the adjustment of several key input values via the settings panel:

Take Profit Multipliers: Users can customize the multipliers for each take-profit level (TP1, TP2, TP3, TP4).

Stop Loss Percentage: The user can also adjust the stop-loss percentage to a custom value.

EMA Periods: The default periods for the EMA 50 and EMA 20 are fixed, but they can be adjusted for different market conditions.

Pros of the Strategy:

EMA Crossover Strategy: A classic and well-known strategy used by traders to identify the start of new trends.

Multiple Take Profit Levels: By taking profits progressively at different levels, the strategy locks in gains as the price moves in favor of the position.

Clear Trend Identification: The use of green and red bars makes it visually easier to follow the market's direction.

Risk Management: The stop-loss and take-profit features help to manage risk and optimize profit-taking.

Cons of the Strategy:

Lagging Indicators: The strategy relies on EMAs, which are lagging indicators. This means that the strategy might enter trades after the trend has already started, leading to missed opportunities or less-than-ideal entry prices.

No Confirmation Indicators: The strategy purely depends on the crossover of two EMAs and does not use other confirming indicators (e.g., RSI, MACD), which might lead to false signals in volatile markets.

How to Use in Real-Time Trading:

Use for Backtesting: Initially, use this strategy in backtest mode to understand how it would have performed historically with your preferred settings.

Paper Trading: Once comfortable, you can use paper trading to test the strategy in real-time market conditions without risking real money.

Live Trading: After testing and optimizing the strategy, you can consider using it for live trading with proper risk management in place (e.g., starting with a small position size and adjusting parameters as needed).

Summary:

This strategy is designed to identify trend reversals using EMA crossovers, with customizable take-profit levels and a stop-loss to manage risk. It's well-suited for traders looking for a systematic way to enter and exit trades based on clear market signals, while also providing flexibility to adjust for different risk profiles and trading styles.

PTS - Bollinger Bands with Trailing StopPTS - Bollinger Bands with Trailing Stop Strategy

Overview

The "PTS - Bollinger Bands with Trailing Stop" strategy is designed to capitalize on strong bullish market movements by combining the Bollinger Bands indicator with a dynamic trailing stop based on the Average True Range (ATR). This strategy aims to enter long positions during upward breakouts and protect profits through an adaptive exit mechanism.

Key Features

1. Bollinger Bands Indicator

Basis Moving Average Type: Choose from SMA, EMA, SMMA, WMA, or VWMA for the Bollinger Bands' basis line. Length: Adjustable period for calculating the moving average and standard deviation (default is 20). Standard Deviation Multiplier (StdDev): Determines the width of the bands (default is 2.0). Source: Select the price data used for calculations (default is the closing price).

2. Entry Conditions

The strategy enters a long position when the closing price crosses above the upper Bollinger Band , indicating strong upward momentum.

3. Exit Conditions

Trailing Stop Loss: Implemented using ATR to adjust dynamically with market volatility. ATR Length: Period for calculating ATR (default is 14). ATR Multiplier for Trailing Stop: Determines how closely the trailing stop follows the price (default is 2.0). Close Below Lower Bollinger Band: The strategy exits the long position if the closing price crosses below the lower Bollinger Band .

4. Risk Management

Commission and Slippage: Commission is set at 0.1%; slippage is set to 3. Position Sizing: Uses 100% of equity per trade (adjustable).

5. Date Range Filter

Specify the time period during which the strategy is active. Start Date: January 1, 2018. End Date: December 31, 2069.

Customizable Inputs

BB Length: Adjust the period for Bollinger Bands calculation. BB StdDev: Modify the standard deviation multiplier. Basis MA Type: Select the moving average type. Source: Choose the price data source. Offset: Shift the Bollinger Bands on the chart. ATR Length: Set the period for ATR calculation. ATR Multiplier for Trailing Stop: Adjust the trailing stop sensitivity.

Thought for 1m 7s

Description for the "PTS - Bollinger Bands with Trailing Stop" Strategy

PTS - Bollinger Bands with Trailing Stop Strategy

Overview

The "PTS - Bollinger Bands with Trailing Stop" strategy is designed to capitalize on strong bullish market movements by combining the Bollinger Bands indicator with a dynamic trailing stop based on the Average True Range (ATR). This strategy aims to enter long positions during upward breakouts and protect profits through an adaptive exit mechanism.

Key Features

1. Bollinger Bands Indicator

Basis Moving Average Type: Choose from SMA, EMA, SMMA, WMA, or VWMA for the Bollinger Bands' basis line. Length: Adjustable period for calculating the moving average and standard deviation (default is 20). Standard Deviation Multiplier (StdDev): Determines the width of the bands (default is 2.0). Source: Select the price data used for calculations (default is the closing price).

2. Entry Conditions

The strategy enters a long position when the closing price crosses above the upper Bollinger Band , indicating strong upward momentum.

3. Exit Conditions

Trailing Stop Loss: Implemented using ATR to adjust dynamically with market volatility. ATR Length: Period for calculating ATR (default is 14). ATR Multiplier for Trailing Stop: Determines how closely the trailing stop follows the price (default is 2.0). Close Below Lower Bollinger Band: The strategy exits the long position if the closing price crosses below the lower Bollinger Band .

4. Risk Management

Commission and Slippage: Commission is set at 0.1%; slippage is set to 3. Position Sizing: Uses 100% of equity per trade (adjustable).

5. Date Range Filter

Specify the time period during which the strategy is active. Start Date: January 1, 2018. End Date: December 31, 2069.

Customizable Inputs

BB Length: Adjust the period for Bollinger Bands calculation. BB StdDev: Modify the standard deviation multiplier. Basis MA Type: Select the moving average type. Source: Choose the price data source. Offset: Shift the Bollinger Bands on the chart. ATR Length: Set the period for ATR calculation. ATR Multiplier for Trailing Stop: Adjust the trailing stop sensitivity.

How the Strategy Works

1. Initialization

Calculates Bollinger Bands and ATR based on selected parameters.

2. Entry Logic

Opens a long position when the closing price exceeds the upper Bollinger Band.

3. Exit Logic

Uses a trailing stop loss based on ATR. Exits if the closing price drops below the lower Bollinger Band.

4. Date Filtering

Executes trades only within the specified date range.

Advantages

Adaptive Risk Management: Trailing stop adjusts to market volatility. Simplicity: Clear entry and exit signals. Customizable Parameters: Tailor the strategy to different assets or conditions.

Considerations

Aggressive Position Sizing: Using 100% equity per trade is high-risk. Market Conditions: Best in trending markets; may produce false signals in sideways markets. Backtesting: Always test on historical data before live trading.

Disclaimer

This strategy is intended for educational and informational purposes only. Trading involves significant risk, and past performance is not indicative of future results. Assess your financial situation and consult a financial advisor if necessary.

Usage Instructions

1. Apply the Strategy: Add it to your TradingView chart. 2. Configure Inputs: Adjust parameters to suit your style and asset. 3. Analyze Backtest Results: Use the Strategy Tester. 4. Optimize Parameters: Experiment with input values. 5. Risk Management: Evaluate position sizing and incorporate risk controls.

Final Notes

The "PTS - Bollinger Bands with Trailing Stop" strategy provides a framework to leverage momentum breakouts while managing risk through adaptive trailing stops. Customize and test thoroughly to align with your trading objectives.

Money Risk Management with Trade Tracking

Overview

The Money Risk Management with Trade Tracking indicator is a powerful tool designed for traders on TradingView to simplify trade simulation and risk management. Unlike the TradingView Strategy Tester, which can be complex for beginners, this indicator provides an intuitive, beginner-friendly interface to evaluate trading strategies in a realistic manner, mirroring real-world trading conditions.

Built on the foundation of open-source contributions from LuxAlgo and TCP, this indicator integrates external indicator signals, overlays take-profit (TP) and stop-loss (SL) levels, and provides detailed money management analytics. It empowers traders to visualize potential profits, losses, and risk-reward ratios, making it easier to understand the financial outcomes of their strategies.

Key Features

Signal Integration: Seamlessly integrates with external long and short signals from other indicators, allowing traders to overlay TP/SL levels based on their preferred strategies.

Realistic Trade Simulation: Simulates trades as they would occur in real-world scenarios, accounting for initial capital, risk percentage, leverage, and compounding effects.

Money Management Dashboard: Displays critical metrics such as current capital, unrealized P&L, risk amount, potential profit, risk-reward ratio, and trade status in a customizable, beginner-friendly table.

TP/SL Visualization: Plots TP and SL levels on the chart with customizable styles (solid, dashed, dotted) and colors, along with optional labels for clarity.

Performance Tracking: Tracks total trades, win/loss counts, win rate, and profit factor, providing a clear overview of strategy performance.

Liquidation Risk Alerts: Warns traders if stop-loss levels risk liquidation based on leverage settings, enhancing risk awareness.

Benefits for Traders

Beginner-Friendly: Simplifies the complexities of the TradingView Strategy Tester, offering an intuitive interface for new traders to simulate and evaluate trades without confusion.

Real-World Insights: Helps traders understand the actual profit or loss potential of their strategies by factoring in capital, risk, and leverage, bridging the gap between theoretical backtesting and real-world execution.

Enhanced Decision-Making: Provides clear, real-time analytics on risk-reward ratios, unrealized P&L, and trade performance, enabling informed trading decisions.

Customizable and Flexible: Allows customization of TP/SL settings, table positions, colors, and sizes, catering to individual trader preferences.

Risk Management Focus: Encourages disciplined trading by highlighting risk amounts, potential profits, and liquidation risks, fostering better financial planning.

Why This Indicator Stands Out

Many traders struggle to translate backtested strategy results into real-world outcomes due to the abstract nature of percentage-based profitability metrics. This indicator addresses that challenge by providing a practical, user-friendly tool that simulates trades with real-world parameters like capital, leverage, and compounding. Its open-source nature ensures accessibility, while its integration with other indicators makes it versatile for various trading styles.

How to Use

Add to TradingView: Copy the Pine Script code into TradingView’s Pine Editor and add it to your chart.

Configure Inputs: Set your initial capital, risk percentage, leverage, and TP/SL values in the indicator settings. Select external long/short signal sources if integrating with other indicators.

Monitor Dashboards: Use the Money Management and Target Dashboard tables to track trade performance and risk metrics in real time.

Analyze Results: Review win rates, profit factors, and P&L to refine your trading strategy.

Credits

This indicator builds upon the open-source contributions of LuxAlgo and TCP , whose efforts in sharing their code have made this tool possible. Their dedication to the trading community is deeply appreciated.

Triangle Breakout Strategy with TP/SL, EMA Filter📌 Triangle Breakout Strategy with TP/SL, EMA Filters, and Backtest – Explained.

✅ 1. Pattern Detection – Triangle Breakout

The script scans for triangle patterns by detecting local pivot highs and pivot lows.

It uses two recent highs and two recent lows to draw converging trendlines (upper and lower boundaries of the triangle).

If the price breaks above the upper trendline, a bullish breakout signal is generated.

🎯 2. TP (Take Profit) & SL (Stop Loss)

When a bullish breakout is detected:

A buy order is placed using strategy.entry.

TP and SL levels are calculated relative to the current close price:

TP = 3% above the entry price

SL = 1.5% below the entry price

These are defined using strategy.exit.

📊 3. EMA Filter

An optional filter checks if:

Price is above both EMA 20 and EMA 50

Only if this condition is met, the strategy allows a long entry.

You can toggle the filter on or off with useEMAFilter.

📈 4. Backtesting with Strategy Tester

This script uses strategy() instead of indicator() to enable TradingView’s built-in backtest engine.

Every buy entry and exit (based on TP or SL) is recorded.

📌 5. Visuals

EMA 20 and EMA 50 lines are plotted on the chart.

A label is shown when a breakout is detected: "Breakout Up"

Results (profit, win rate, drawdown, etc.) can be viewed in the Strategy Tester panel.

RiskMetrics█ OVERVIEW

This library is a tool for Pine programmers that provides functions for calculating risk-adjusted performance metrics on periodic price returns. The calculations used by this library's functions closely mirror those the Broker Emulator uses to calculate strategy performance metrics (e.g., Sharpe and Sortino ratios) without depending on strategy-specific functionality.

█ CONCEPTS

Returns, risk, and volatility

The return on an investment is the relative gain or loss over a period, often expressed as a percentage. Investment returns can originate from several sources, including capital gains, dividends, and interest income. Many investors seek the highest returns possible in the quest for profit. However, prudent investing and trading entails evaluating such returns against the associated risks (i.e., the uncertainty of returns and the potential for financial losses) for a clearer perspective on overall performance and sustainability.

One way investors and analysts assess the risk of an investment is by analyzing its volatility , i.e., the statistical dispersion of historical returns. Investors often use volatility in risk estimation because it provides a quantifiable way to gauge the expected extent of fluctuation in returns. Elevated volatility implies heightened uncertainty in the market, which suggests higher expected risk. Conversely, low volatility implies relatively stable returns with relatively minimal fluctuations, thus suggesting lower expected risk. Several risk-adjusted performance metrics utilize volatility in their calculations for this reason.

Risk-free rate

The risk-free rate represents the rate of return on a hypothetical investment carrying no risk of financial loss. This theoretical rate provides a benchmark for comparing the returns on a risky investment and evaluating whether its excess returns justify the risks. If an investment's returns are at or below the theoretical risk-free rate or the risk premium is below a desired amount, it may suggest that the returns do not compensate for the extra risk, which might be a call to reassess the investment.

Since the risk-free rate is a theoretical concept, investors often utilize proxies for the rate in practice, such as Treasury bills and other government bonds. Conventionally, analysts consider such instruments "risk-free" for a domestic holder, as they are a form of government obligation with a low perceived likelihood of default.

The average yield on short-term Treasury bills, influenced by economic conditions, monetary policies, and inflation expectations, has historically hovered around 2-3% over the long term. This range also aligns with central banks' inflation targets. As such, one may interpret a value within this range as a minimum proxy for the risk-free rate, as it may correspond to the minimum rate required to maintain purchasing power over time.

The built-in Sharpe and Sortino ratios that strategies calculate and display in the Performance Summary tab use a default risk-free rate of 2%, and the metrics in this library's example code use the same default rate. Users can adjust this value to fit their analysis needs.

Risk-adjusted performance

Risk-adjusted performance metrics gauge the effectiveness of an investment by considering its returns relative to the perceived risk. They aim to provide a more well-rounded picture of performance by factoring in the level of risk taken to achieve returns. Investors can utilize such metrics to help determine whether the returns from an investment justify the risks and make informed decisions.

The two most commonly used risk-adjusted performance metrics are the Sharpe ratio and the Sortino ratio.

1. Sharpe ratio

The Sharpe ratio , developed by Nobel laureate William F. Sharpe, measures the performance of an investment compared to a theoretically risk-free asset, adjusted for the investment risk. The ratio uses the following formula:

Sharpe Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑎

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑎 = Standard deviation of the investment's returns (volatility)

A higher Sharpe ratio indicates a more favorable risk-adjusted return, as it signifies that the investment produced higher excess returns per unit of increase in total perceived risk.

2. Sortino ratio

The Sortino ratio is a modified form of the Sharpe ratio that only considers downside volatility , i.e., the volatility of returns below the theoretical risk-free benchmark. Although it shares close similarities with the Sharpe ratio, it can produce very different values, especially when the returns do not have a symmetrical distribution, since it does not penalize upside and downside volatility equally. The ratio uses the following formula:

Sortino Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑑

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑑 = Downside deviation (standard deviation of negative excess returns, or downside volatility)

The Sortino ratio offers an alternative perspective on an investment's return-generating efficiency since it does not consider upside volatility in its calculation. A higher Sortino ratio signifies that the investment produced higher excess returns per unit of increase in perceived downside risk.

█ CALCULATIONS

Return period detection

Calculating risk-adjusted performance metrics requires collecting returns across several periods of a given size. Analysts may use different period sizes based on the context and their preferences. However, two widely used standards are monthly or daily periods, depending on the available data and the investment's duration. The built-in ratios displayed in the Strategy Tester utilize returns from either monthly or daily periods in their calculations based on the following logic:

• Use monthly returns if the history of closed trades spans at least two months.

• Use daily returns if the trades span at least two days but less than two months.

• Do not calculate the ratios if the trade data spans fewer than two days.

This library's `detectPeriod()` function applies related logic to available chart data rather than trade data to determine which period is appropriate:

• It returns true if the chart's data spans at least two months, indicating that it's sufficient to use monthly periods.

• It returns false if the chart's data spans at least two days but not two months, suggesting the use of daily periods.

• It returns na if the length of the chart's data covers less than two days, signifying that the data is insufficient for meaningful ratio calculations.

It's important to note that programmers should only call `detectPeriod()` from a script's global scope or within the outermost scope of a function called from the global scope, as it requires the time value from the first bar to accurately measure the amount of time covered by the chart's data.

Collecting periodic returns

This library's `getPeriodicReturns()` function tracks price return data within monthly or daily periods and stores the periodic values in an array . It uses a `detectPeriod()` call as the condition to determine whether each element in the array represents the return over a monthly or daily period.

The `getPeriodicReturns()` function has two overloads. The first overload requires two arguments and outputs an array of monthly or daily returns for use in the `sharpe()` and `sortino()` methods. To calculate these returns:

1. The `percentChange` argument should be a series that represents percentage gains or losses. The values can be bar-to-bar return percentages on the chart timeframe or percentages requested from a higher timeframe.

2. The function compounds all non-na `percentChange` values within each monthly or daily period to calculate the period's total return percentage. When the `percentChange` represents returns from a higher timeframe, ensure the requested data includes gaps to avoid compounding redundant values.

3. After a period ends, the function queues the compounded return into the array , removing the oldest element from the array when its size exceeds the `maxPeriods` argument.

The resulting array represents the sequence of closed returns over up to `maxPeriods` months or days, depending on the available data.

The second overload of the function includes an additional `benchmark` parameter. Unlike the first overload, this version tracks and collects differences between the `percentChange` and the specified `benchmark` values. The resulting array represents the sequence of excess returns over up to `maxPeriods` months or days. Passing this array to the `sharpe()` and `sortino()` methods calculates generalized Information ratios , which represent the risk-adjustment performance of a sequence of returns compared to a risky benchmark instead of a risk-free rate. For consistency, ensure the non-na times of the `benchmark` values align with the times of the `percentChange` values.

Ratio methods

This library's `sharpe()` and `sortino()` methods respectively calculate the Sharpe and Sortino ratios based on an array of returns compared to a specified annual benchmark. Both methods adjust the annual benchmark based on the number of periods per year to suit the frequency of the returns:

• If the method call does not include a `periodsPerYear` argument, it uses `detectPeriod()` to determine whether the returns represent monthly or daily values based on the chart's history. If monthly, the method divides the `annualBenchmark` value by 12. If daily, it divides the value by 365.

• If the method call does specify a `periodsPerYear` argument, the argument's value supersedes the automatic calculation, facilitating custom benchmark adjustments, such as dividing by 252 when analyzing collected daily stock returns.

When the array passed to these methods represents a sequence of excess returns , such as the result from the second overload of `getPeriodicReturns()`, use an `annualBenchmark` value of 0 to avoid comparing those excess returns to a separate rate.

By default, these methods only calculate the ratios on the last available bar to minimize their resource usage. Users can override this behavior with the `forceCalc` parameter. When the value is true , the method calculates the ratio on each call if sufficient data is available, regardless of the bar index.

Look first. Then leap.

█ FUNCTIONS & METHODS

This library contains the following functions:

detectPeriod()

Determines whether the chart data has sufficient coverage to use monthly or daily returns

for risk metric calculations.

Returns: (bool) `true` if the period spans more than two months, `false` if it otherwise spans more

than two days, and `na` if the data is insufficient.

getPeriodicReturns(percentChange, maxPeriods)

(Overload 1 of 2) Tracks periodic return percentages and queues them into an array for ratio

calculations. The span of the chart's historical data determines whether the function uses

daily or monthly periods in its calculations. If the chart spans more than two months,

it uses "1M" periods. Otherwise, if the chart spans more than two days, it uses "1D"

periods. If the chart covers less than two days, it does not store changes.

Parameters:

percentChange (float) : (series float) The change percentage. The function compounds non-na values from each

chart bar within monthly or daily periods to calculate the periodic changes.

maxPeriods (simple int) : (simple int) The maximum number of periodic returns to store in the returned array.

Returns: (array) An array containing the overall percentage changes for each period, limited

to the maximum specified by `maxPeriods`.

getPeriodicReturns(percentChange, benchmark, maxPeriods)

(Overload 2 of 2) Tracks periodic excess return percentages and queues the values into an

array. The span of the chart's historical data determines whether the function uses

daily or monthly periods in its calculations. If the chart spans more than two months,

it uses "1M" periods. Otherwise, if the chart spans more than two days, it uses "1D"

periods. If the chart covers less than two days, it does not store changes.

Parameters:

percentChange (float) : (series float) The change percentage. The function compounds non-na values from each

chart bar within monthly or daily periods to calculate the periodic changes.

benchmark (float) : (series float) The benchmark percentage to compare against `percentChange` values.

The function compounds non-na values from each bar within monthly or

daily periods and subtracts the results from the compounded `percentChange` values to

calculate the excess returns. For consistency, ensure this series has a similar history

length to the `percentChange` with aligned non-na value times.

maxPeriods (simple int) : (simple int) The maximum number of periodic excess returns to store in the returned array.

Returns: (array) An array containing monthly or daily excess returns, limited

to the maximum specified by `maxPeriods`.

method sharpeRatio(returnsArray, annualBenchmark, forceCalc, periodsPerYear)

Calculates the Sharpe ratio for an array of periodic returns.

Callable as a method or a function.

Namespace types: array

Parameters:

returnsArray (array) : (array) An array of periodic return percentages, e.g., returns over monthly or

daily periods.

annualBenchmark (float) : (series float) The annual rate of return to compare against `returnsArray` values. When

`periodsPerYear` is `na`, the function divides this value by 12 to calculate a

monthly benchmark if the chart's data spans at least two months or 365 for a daily

benchmark if the data otherwise spans at least two days. If `periodsPerYear`

has a specified value, the function divides the rate by that value instead.

forceCalc (bool) : (series bool) If `true`, calculates the ratio on every call. Otherwise, ratio calculation

only occurs on the last available bar. Optional. The default is `false`.

periodsPerYear (simple int) : (simple int) If specified, divides the annual rate by this value instead of the value

determined by the time span of the chart's data.

Returns: (float) The Sharpe ratio, which estimates the excess return per unit of total volatility.

method sortinoRatio(returnsArray, annualBenchmark, forceCalc, periodsPerYear)

Calculates the Sortino ratio for an array of periodic returns.

Callable as a method or a function.

Namespace types: array

Parameters:

returnsArray (array) : (array) An array of periodic return percentages, e.g., returns over monthly or

daily periods.

annualBenchmark (float) : (series float) The annual rate of return to compare against `returnsArray` values. When

`periodsPerYear` is `na`, the function divides this value by 12 to calculate a

monthly benchmark if the chart's data spans at least two months or 365 for a daily

benchmark if the data otherwise spans at least two days. If `periodsPerYear`

has a specified value, the function divides the rate by that value instead.

forceCalc (bool) : (series bool) If `true`, calculates the ratio on every call. Otherwise, ratio calculation

only occurs on the last available bar. Optional. The default is `false`.

periodsPerYear (simple int) : (simple int) If specified, divides the annual rate by this value instead of the value

determined by the time span of the chart's data.

Returns: (float) The Sortino ratio, which estimates the excess return per unit of downside

volatility.

Bitcoin Momentum StrategyThis is a very simple long-only strategy I've used since December 2022 to manage my Bitcoin position.

I'm sharing it as an open-source script for other traders to learn from the code and adapt it to their liking if they find the system concept interesting.

General Overview

Always do your own research and backtesting - this script is not intended to be traded blindly (no script should be) and I've done limited testing on other markets beyond Ethereum and BTC, it's just a template to tweak and play with and make into one's own.

The results shown in the strategy tester are from Bitcoin's inception so as to get a large sample size of trades, and potential returns have diminished significantly as BTC has grown to become a mega cap asset, but the script includes a date filter for backtesting and it has still performed solidly in recent years (speaking from personal experience using it myself - DYOR with the date filter).

The main advantage of this system in my opinion is in limiting the max drawdown significantly versus buy & hodl. Theoretically much better returns can be made by just holding, but that's also a good way to lose 70%+ of your capital in the inevitable bear markets (also speaking from experience).

In saying all of that, the future is fundamentally unknowable and past results in no way guarantee future performance.

System Concept:

Capture as much Bitcoin upside volatility as possible while side-stepping downside volatility as quickly as possible.

The system uses a simple but clever momentum-style trailing stop technique I learned from one of my trading mentors who uses this approach on momentum/trend-following stock market systems.

Basically, the system "ratchets" up the stop-loss to be much tighter during high bearish volatility to protect open profits from downside moves, but loosens the stop loss during sustained bullish momentum to let the position ride.

It is invested most of the time, unless BTC is trading below its 20-week EMA in which case it stays in cash/USDT to avoid holding through bear markets. It only trades one position (no pyramiding) and does not trade short, but can easily be tweaked to do whatever you like if you know what you're doing in Pine.

Default parameters:

HTF: Weekly Chart

EMA: 20-Period

ATR: 5-period

Bar Lookback: 7

Entry Rule #1:

Bitcoin's current price must be trading above its higher-timeframe EMA (Weekly 20 EMA).

Entry Rule #2:

Bitcoin must not be in 'caution' condition (no large bearish volatility swings recently).

Enter at next bar's open if conditions are met and we are not already involved in a trade.

"Caution" Condition:

Defined as true if BTC's recent 7-bar swing high minus current bar's low is > 1.5x ATR, or Daily close < Daily 20-EMA.

Trailing Stop:

Stop is trailed 1 ATR from recent swing high, or 20% of ATR if in caution condition (ie. 0.2 ATR).

Exit on next bar open upon a close below stop loss.

I typically use a limit order to open & exit trades as close to the open price as possible to reduce slippage, but the strategy script uses market orders.

I've never had any issues getting filled on limit orders close to the market price with BTC on the Daily timeframe, but if the exchange has relatively low slippage I've found market orders work fine too without much impact on the results particularly since BTC has consistently remained above $20k and highly liquid.

Cost of Trading:

The script uses no leverage and a default total round-trip commission of 0.3% which is what I pay on my exchange based on their tier structure, but this can vary widely from exchange to exchange and higher commission fees will have a significantly negative impact on realized gains so make sure to always input the correct theoretical commission cost when backtesting any script.

Static slippage is difficult to estimate in the strategy tester given the wide range of prices & liquidity BTC has experienced over the years and it largely depends on position size, I set it to 150 points per buy or sell as BTC is currently very liquid on the exchange I trade and I use limit orders where possible to enter/exit positions as close as possible to the market's open price as it significantly limits my slippage.

But again, this can vary a lot from exchange to exchange (for better or worse) and if BTC volatility is high at the time of execution this can have a negative impact on slippage and therefore real performance, so make sure to adjust it according to your exchange's tendencies.

Tax considerations should also be made based on short-term trade frequency if crypto profits are treated as a CGT event in your region.

Summary:

A simple, but effective and fairly robust system that achieves the goals I set for it.

From my preliminary testing it appears it may also work on altcoins but it might need a bit of tweaking/loosening with the trailing stop distance as the default parameters are designed to work with Bitcoin which obviously behaves very differently to smaller cap assets.

Good luck out there!

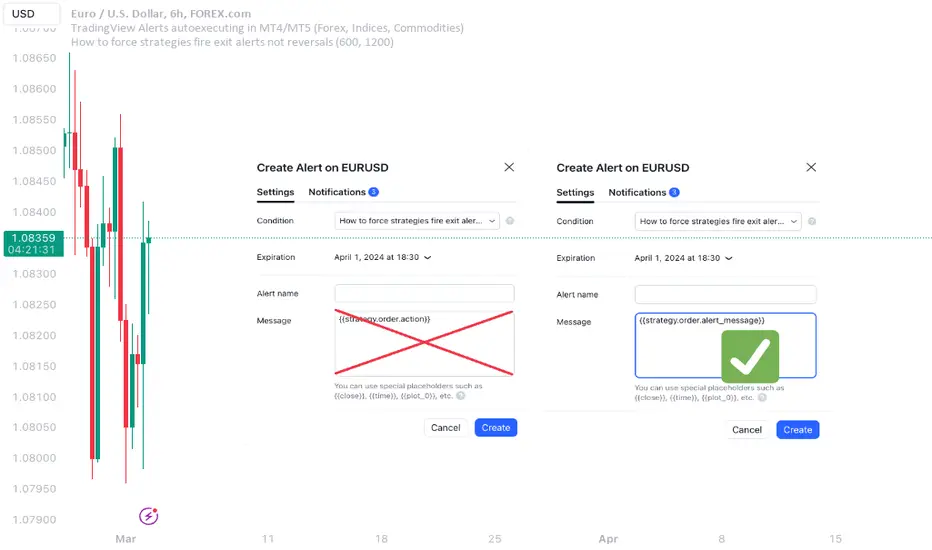

How to force strategies fire exit alerts not reversalsPineScript has gone a long way, from very simple and little-capable scripting language to a robust coding platform with reliable execution endpoints. However, this one small intuitivity glitch is still there and is likely to stay, because it is traditionally justified and quite intuitive for significant group of traders. I'm sharing this workaround in response to frequent inquiries about it.

What's the glitch? When setting alerts on strategies to be synchronized with TradingView's Strategy Tester events, using simple alert messages such as "buy" or "sell" based on entry direction seems straightforward by inserting {{strategy.order.action}} into the Create Alert's "Message" field. Because "buy" or "sell" are exactly the strings produced by {{strategy.order.action}} placeholder. However, complications arise when attempting to EXIT positions without reversing, whether triggered by price levels like Stop Loss or Take Profit, or logical conditions to close trades. Those bricks fall apart, because on such events {{strategy.order.action}} sends the same "sell" for exiting buy positions and "buy" for exiting sell positions, instead of something more differentiating like "closebuy" or "closesell". As a result reversal trades are opened, instead of simply closing the open ones.

This convention harkens back to traditional stock market practices, where traders either bought shares to enter positions or sold them to exit. However, modern trading encompasses diverse instruments like CFDs, indices, and Forex, alongside advanced features such as Stop Loss, reshaping the landscape. Despite these advancements, the traditional nomenclature persists.

And is poised to stay on TradingView as well, so we need a workaround to get a simple strategy going. Luckily it is here and is called alert_message . It is a parameter, which needs to be added into each strategy.entry() / strategy.exit() / strategy.close() function call - each call, which causes Strategy Tester to produce entry or exit orders. As in this example script:

line 12: strategy.entry(... alert_message ="buy")

line 14: strategy.entry(... alert_message ="sell")

line 19: strategy.exit(... alert_message ="closebuy")

line 20: strategy.exit(... alert_message ="closesell")

line 24: strategy.close(... alert_message ="closebuy")

line 26: strategy.close(... alert_message ="closesell")

These alert messages are compatible with the Alerts Syntax of TradingConnector - a tool facilitating auto-execution of TradingView alerts in MetaTrader 4 or 5. Yes, simple alert messages like "buy" / "sell" / "closebuy" / "closesell" suffice to carry the execution of simple strategy, without complex JSON files with multiple ids and such. Other parameters can be added (actually plenty), but they are only option and that's not a part of this story :)

Last thing left to do is to replace "Message" in Create Alert popup with {{strategy.order.alert_message}} . This placeholder transmits the string defined in the PineScript alert_message= parameter, as outlined in this publication. With this workaround, executing closing alerts becomes seamless within PineScript strategies on TradingView.

Disclaimer: this content is purely educational, especially please don't pay attention to backtest results on any timeframe/ticker.

LANZ Strategy 5.0 [Backtest]🔷 LANZ Strategy 5.0 — Rule-Based BUY Logic with Time Filter, Session Limits and Auto SL/TP Execution

This is the backtest version of LANZ Strategy 5.0, built as a strategy script to evaluate real performance under fixed intraday conditions. It automatically places BUY and SELL trades based on structured candle confirmation, EMA trend alignment, and session-based filters. The system simulates real-time execution with precise Stop Loss and Take Profit levels.

📌 Built for traders seeking to simulate clean intraday logic with fully automated entries and performance metrics.

🧠 Core Logic & Strategy Conditions

✅ BUY Signal Conditions:

Price is above the EMA200

The last 3 candles are bullish (close > open)

The signal occurs within the defined session window (NY time)

Daily trade limit has not been exceeded

If all are true, a BUY order is executed at market, with SL and TP set immediately.

🔻 SELL Signal Conditions (Optional):

Exactly inverse to BUY (below EMA + 3 bearish candles). Disabled by default.

🕐 Operational Time Filter (New York Time)

You can fully customize your intraday window:

Start Time: e.g., 01:15 NY

End Time: e.g., 16:00 NY

The system evaluates signals only within this range, even across midnight if configured.

🔁 Trade Management System

One trade at a time per signal

Trades include a Stop Loss (SL) and Take Profit (TP) based on pip distance

Trade result is calculated automatically

Each signal is shown with a triangle marker (BUY only, by default)

🧪 Backtest Accuracy

This version uses:

strategy.order() for entries

strategy.exit() for SL and TP

strategy.close_all() at the configured manual closing time

This ensures realistic behavior in the TradingView strategy tester.

⚙️ Flow Summary (Step-by-Step)

On every bar, check:

Is the time within the operational session?

Is the price above the EMA?

Are the last 3 candles bullish?

If conditions met → A BUY trade is opened:

SL = entry – X pips

TP = entry + Y pips

Trade closes:

If SL or TP is hit

Or at the configured manual close time (e.g., 16:00 NY)

📊 Settings Overview

Timeframe: 1-hour (ideal)

SL/TP: Configurable in pips

Max trades/day: User-defined (default = 99 = unlimited)

Manual close: Adjustable by time

Entry type: Market (not limit)

Visuals: Plotshape triangle for BUY entry

👨💻 Credits:

💡 Developed by: LANZ

🧠 Strategy logic & execution: LANZ

✅ Designed for: Clean backtesting, clarity in execution, and intraday logic simulation

Donchian Quest Research// =================================

Trend following strategy.

// =================================

Strategy uses two channels. One channel - for opening trades. Second channel - for closing.

Channel is similar to Donchian channel, but uses Close prices (not High/Low). That helps don't react to wicks of volatile candles (“stop hunting”). In most cases openings occur earlier than in Donchian channel. Closings occur only for real breakout.

// =================================

Strategy waits for beginning of trend - when price breakout of channel. Default length of both channels = 50 candles.

Conditions of trading:

- Open Long: If last Close = max Close for 50 closes.

- Close Long: If last Close = min Close for 50 closes.

- Open Short: If last Close = min Close for 50 closes.

- Close Short: If last Close = max Close for 50 closes.

// =================================

Color of lines:

- black - channel for opening trade.

- red - channel for closing trade.

- yellow - entry price.

- fuchsia - stoploss and breakeven.

- vertical green - go Long.

- vertical red - go Short.

- vertical gray - close in end, don't trade anymore.

// =================================

Order size calculated with ATR and volatility.

You can't trade 1 contract in BTC and 1 contract in XRP - for example. They have different price and volatility, so 1 contract BTC not equal 1 contract XRP.

Script uses universal calculation for every market. It is based on:

- Risk - USD sum you ready to loss in one trade. It calculated as percent of Equity.

- ATR indicator - measurement of volatility.

With default setting your stoploss = 0.5 percent of equity:

- If initial capital is 1000 USD and used parameter "Permit stop" - loss will be 5 USD (0.5 % of equity).

- If your Equity rises to 2000 USD and used parameter "Permit stop"- loss will be 10 USD (0.5 % of Equity).

// =================================

This Risk works only if you enable “Permit stop” parameter in Settings.

If this parameter disabled - strategy works as reversal strategy:

⁃ If close Long - channel border works as stoploss and momentarily go Short.

⁃ If close Short - channel border works as stoploss and momentarily go Long.

Channel borders changed dynamically. So sometime your loss will be greater than ‘Risk %’. Sometime - less than ‘Risk %’.

If this parameter enabled - maximum loss always equal to 'Risk %'. This parameter also include breakeven: if profit % = Risk %, then move stoploss to entry price.

// =================================

Like all trend following strategies - it works only in trend conditions. If no trend - slowly bleeding. There is no special additional indicator to filter trend/notrend. You need to trade every signal of strategy.

Strategy gives many losses:

⁃ 30 % of trades will close with profit.

⁃ 70 % of trades will close with loss.

⁃ But profit from 30% will be much greater than loss from 70 %.

Your task - patiently wait for it and don't use risky setting for position sizing.

// =================================

Recommended timeframe - Daily.

// =================================

Trend can vary in lengths. Selecting length of channels determine which trend you will be hunting:

⁃ 20/10 - from several days to several weeks.

⁃ 20/20 or 50/20 - from several weeks to several months.

⁃ 50/50 or 100/50 or 100/100 - from several months to several years.

// =================================

Inputs (Settings):

- Length: length of channel for trade opening/closing. You can choose 20/10, 20/20, 50/20, 50/50, 100/50, 100/100. Default value: 50/50.

- Permit Long / Permit short: Longs are most profitable for this strategy. You can disable Shorts and enable Longs only. Default value: permit all directions.

- Risk % of Equity: for position sizing used Equity percent. Don't use values greater than 5 % - it's risky. Default value: 0.5%.

⁃ ATR multiplier: this multiplier moves stoploss up or down. Big multiplier = small size of order, small profit, stoploss far from entry, low chance of stoploss. Small multiplier = big size of order, big profit, stop near entry, high chance of stoploss. Default value: 2.

- ATR length: number of candles to calculate ATR indicator. It used for order size and stoploss. Default value: 20.

- Close in end - to close active trade in the end (and don't trade anymore) or leave it open. You can see difference in Strategy Tester. Default value: don’t close.

- Permit stop: use stop or go reversal. Default value: without stop, reversal strategy.

// =================================

Properties (Settings):

- Initial capital - 1000 USD.

- Script don't uses 'Order size' - you need to change 'Risk %' in Inputs instead.

- Script don't uses 'Pyramiding'.

- 'Commission' 0.055 % and 'Slippage' 0 - this parameters are for crypto exchanges with perpetual contracts (for example Bybit). If use on other markets - set it accordingly to your exchange parameters.

// =================================

Big dataset used for chart - 'BITCOIN ALL TIME HISTORY INDEX'. It gives enough trades to understand logic of script. It have several good trends.

// =================================

XTZ trading strategy for Bear monthsThis is my 3rd approach into trading XTZ. It is tuned into bear months and needs to work for at least 30 days.

It looks at the rebalance oscillator and bear market indicator and tries to find a position in the market that does not lose money within the month.

Use the cog icon to update the trading window to fit previous months, and check out the data window for its real performance. Do not rely on the Strategy Tester since this strategy is performing only with `strategy.order` making the values of the Strategy Tester irrelevant and inconsistent with its performance.

Zendog V2 backtest DCA bot 3commasHi everyone,

After a few iterations and additional implemented features this version of the Backtester is now open source.

The Strategy is a Backtester for 3commas DCA bots. The main usage scenario is to plugin your external indicator, and backtest it using different DCA settings.

Before using this script please make sure you read these explanations and make sure you understand how it works.

Features:

- Because of Tradingview limitations on how orders are grouped into Trades, this Strategy statistics are calculated by the script, so please ignore the Strategy Tester statistics completely

Statistics Table explained:

- Status: either all deals are closed or there is a deal still running, in which case additional info

is provided below, as when the deal started, current PnL, current SO

- Finished deals: Total number of closed deals both Winning and Losing.

A deal is comprised as the Base Order (BO) + all Safety Orders (SO) related to that deal, so this number

will be different than the Strategy Tester List of Trades

- Winning Deals: Deal ended in profit

- Losing deals: Deals ended with loss due to Stop Loss. In the future I might add a Deal Stop condition to

the script, so that will count towards this number as well.

- Total days ( Max / Avg days in Deal ):

Total Days in the Backtest given by either Tradingview limitation on the number of candles or by the

config of the script regarding "Limit Date Range".

Max Days spent in a deal + which period this happened.

Avg days spent in a deal.

- Required capital: This is the total capital required to run the Backtester and it is automatically calculated by

the script taking into consideration BO size, SO size, SO volume scale. This should be the same as 3commas.

This number overwrites strategy.initial_capital and is used to calculate Profit and other stats, so you don't need

to update strategy.initial_capital every time you change BO/SO settings

- Profit after commission

- Buy and Hold return: The PnL that could have been obtained by buying at the close of the first candle of the

backtester and selling at the last.

- Covered deviation: The % of price move from initial BO order covered by SO settings

- Max Deviation: Biggest market % price move vs BO price, in the other direction (for long

is down, for short it is up)

- Max Drawdown: Biggest market % price move vs Avg price of the whole Trade (BO + any SO), in the other

direction (for long price goes down, for short it goes up)

This is calculated for the whole Trade so it is different than List of Trades

- Max / Avg bars in deal

- Total volume / Commission calculated by the strategy. For correct commission please set Commission in the

Inputs Tab and you may ignore Properties Tab

- Close stats for deals: This is a list of how many Trades were closed at each step, including Stop Loss (if

configured), together with covered deviation for that step, the number of deals, and the percentage of this

number from all the deals

TODO: Might add deal avg value for each step

- Settings Table that can be enabled / disabled just to have an overview of your configs on the chart, this is a

drawn on bottom left

- Steps Table similar to 3commas, this is also drawn on bottom left, so please disable Settings table if you want

to see this one

TODO: Might add extra stats here

- Deal start condition: built in RSI-7 or plugin any external indicator and compare with any value the indicator plots

(main purpose of this strategy is to connect your own studies, so using external indicator is recommended)

- Base order and safety orders configs similar to 3commas (order size, percent deviation, safety orders,

percent scale and volume scale)

- Long and Short

- Stop Loss

- Support for Take profit from base order or from Total volume of the deal

- Configs help (besides self explanatory):

- Chart theme: Adjust according to the theme you run on. There is no way to detect theme at the moment.

This adjust different colors

- Deal Start Type: Either a builtin RSI7 or "External indicator"

- Indicator Source an value: If using External Indicator then select source, comparison and value.

For example you could start a deal when Volume is greater than xxxx, or code a custom indicator that plots

different values based on your conditions and test those values

- Visuals / Decimals for display: Adjust according to your symbol

- BO Entry Price for steps table: This is the BO start deal price used to calculate the steps in the table

Inferential Statistics And Quick Metrics For Strategy Analysis.Part of this script is used to calculate inferential statistics and metrics not available through the built in variables in the strategy tester.

A label will be created on the last bar displaying important strategy results, so you can test and analyze strategies quicker.

The built in strategy itself is just an example. You can copy and paste the metrics into any existing version 4 strategy and instantly use it**

**Just be sure all the variable names are unique in your target script.

I am looking for critique and would appreciate input on the statistical functions. I am aware that some of these functions are based on the assumption that the data is normally distributed. It's not meant to be perfect, but it is meant to be helpful. So if you think I can add or improve something to make it more helpful, let me know.

RSI Strategy With TP/SL - Lower TFThis Pine Script strategy integrates the Relative Strength Index (RSI) for trade signals with user-defined Take Profit (TP) and Stop Loss (SL) levels. It's designed for flexible application in different market conditions, offering long, short, or dual-direction trading.

Short Description

The strategy uses the RSI to identify overbought and oversold market conditions:

Buy signal: When RSI drops below the specified "Buy Level."

Sell signal: When RSI rises above the "Sell Level."

Additionally, it manages risk and profit targets with:

Take Profit (TP): Exits trades when the price reaches a percentage gain.

Stop Loss (SL): Exits trades to limit losses if the price falls by a certain percentage.

The strategy is versatile and includes options for visualizing performance, monthly profit/loss data, and detailed trade metrics.

How to Use

Set Parameters:

RSI Period: Default is 14. Adjust based on your analysis.

RSI Buy/Sell Levels:

Buy Level: Default is 40. Consider higher levels for conservative entries.

Sell Level: Default is 60. Lower this for earlier exits.

Take Profit (%): Set your profit target (default: 5%).

Stop Loss (%): Set your risk tolerance (default: 2%).

Trade Direction: Choose "Long Only," "Short Only," or "Both."

Interpret Signals:

Buy signals appear when RSI crosses below the buy threshold.

Sell signals appear when RSI crosses above the sell threshold.

Risk Management:

The strategy dynamically calculates TP and SL levels for each trade.

TP/SL is applied using the percentage input based on the entry price.

Monitor Performance:

Review trade statistics in the "Strategy Tester."

Use the monthly performance table to track P/L across months.

Customize Alerts:

Alerts for buy, sell, TP, and SL events can be used to automate notifications.

Key Features

Configurable RSI Settings: Adaptable to various market conditions.

Risk Management: Built-in TP and SL management.

Customizable Trade Direction: Tailored for long-only, short-only, or both directions.

Monthly P/L Table: Visualizes performance trends over time.

Alerts: Notifies when critical trade events occur.

Please do your own research before ase this to your real trading.

JordanSwindenLibraryLibrary "JordanSwindenLibrary"

TODO: add library description here

getDecimals()

Calculates how many decimals are on the quote price of the current market

Returns: The current decimal places on the market quote price

getPipSize(multiplier)

Calculates the pip size of the current market

Parameters:

multiplier (int) : The mintick point multiplier (1 by default, 10 for FX/Crypto/CFD but can be used to override when certain markets require)

Returns: The pip size for the current market

truncate(number, decimalPlaces)

Truncates (cuts) excess decimal places

Parameters:

number (float) : The number to truncate

decimalPlaces (simple float) : (default=2) The number of decimal places to truncate to

Returns: The given number truncated to the given decimalPlaces

toWhole(number)

Converts pips into whole numbers

Parameters:

number (float) : The pip number to convert into a whole number

Returns: The converted number

toPips(number)

Converts whole numbers back into pips

Parameters:

number (float) : The whole number to convert into pips

Returns: The converted number

getPctChange(value1, value2, lookback)

Gets the percentage change between 2 float values over a given lookback period

Parameters:

value1 (float) : The first value to reference

value2 (float) : The second value to reference

lookback (int) : The lookback period to analyze

Returns: The percent change over the two values and lookback period

random(minRange, maxRange)

Wichmann–Hill Pseudo-Random Number Generator

Parameters:

minRange (float) : The smallest possible number (default: 0)

maxRange (float) : The largest possible number (default: 1)

Returns: A random number between minRange and maxRange

bullFib(priceLow, priceHigh, fibRatio)

Calculates a bullish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

bearFib(priceLow, priceHigh, fibRatio)

Calculates a bearish fibonacci value

Parameters:

priceLow (float) : The lowest price point

priceHigh (float) : The highest price point

fibRatio (float) : The fibonacci % ratio to calculate

Returns: The fibonacci value of the given ratio between the two price points

getMA(length, maType)

Gets a Moving Average based on type (! MUST BE CALLED ON EVERY TICK TO BE ACCURATE, don't place in scopes)

Parameters:

length (simple int) : The MA period

maType (string) : The type of MA

Returns: A moving average with the given parameters

barsAboveMA(lookback, ma)

Counts how many candles are above the MA

Parameters:

lookback (int) : The lookback period to look back over

ma (float) : The moving average to check

Returns: The bar count of how many recent bars are above the MA

barsBelowMA(lookback, ma)

Counts how many candles are below the MA

Parameters:

lookback (int) : The lookback period to look back over

ma (float) : The moving average to reference

Returns: The bar count of how many recent bars are below the EMA

barsCrossedMA(lookback, ma)

Counts how many times the EMA was crossed recently (based on closing prices)

Parameters:

lookback (int) : The lookback period to look back over

ma (float) : The moving average to reference

Returns: The bar count of how many times price recently crossed the EMA (based on closing prices)

getPullbackBarCount(lookback, direction)

Counts how many green & red bars have printed recently (ie. pullback count)

Parameters:

lookback (int) : The lookback period to look back over

direction (int) : The color of the bar to count (1 = Green, -1 = Red)

Returns: The bar count of how many candles have retraced over the given lookback & direction

getBodySize()

Gets the current candle's body size (in POINTS, divide by 10 to get pips)

Returns: The current candle's body size in POINTS

getTopWickSize()

Gets the current candle's top wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's top wick size in POINTS

getBottomWickSize()

Gets the current candle's bottom wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's bottom wick size in POINTS

getBodyPercent()

Gets the current candle's body size as a percentage of its entire size including its wicks

Returns: The current candle's body size percentage

isHammer(fib, colorMatch)

Checks if the current bar is a hammer candle based on the given parameters

Parameters:

fib (float) : (default=0.382) The fib to base candle body on

colorMatch (bool) : (default=false) Does the candle need to be green? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a hammer candle

isStar(fib, colorMatch)

Checks if the current bar is a shooting star candle based on the given parameters

Parameters:

fib (float) : (default=0.382) The fib to base candle body on

colorMatch (bool) : (default=false) Does the candle need to be red? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a shooting star candle

isDoji(wickSize, bodySize)

Checks if the current bar is a doji candle based on the given parameters

Parameters:

wickSize (float) : (default=2) The maximum top wick size compared to the bottom (and vice versa)

bodySize (float) : (default=0.05) The maximum body size as a percentage compared to the entire candle size

Returns: A boolean - true if the current bar matches the requirements of a doji candle

isBullishEC(allowance, rejectionWickSize, engulfWick)

Checks if the current bar is a bullish engulfing candle

Parameters:

allowance (float) : (default=0) How many POINTS to allow the open to be off by (useful for markets with micro gaps)

rejectionWickSize (float) : (default=disabled) The maximum rejection wick size compared to the body as a percentage

engulfWick (bool) : (default=false) Does the engulfing candle require the wick to be engulfed as well?

Returns: A boolean - true if the current bar matches the requirements of a bullish engulfing candle

isBearishEC(allowance, rejectionWickSize, engulfWick)

Checks if the current bar is a bearish engulfing candle

Parameters:

allowance (float) : (default=0) How many POINTS to allow the open to be off by (useful for markets with micro gaps)

rejectionWickSize (float) : (default=disabled) The maximum rejection wick size compared to the body as a percentage

engulfWick (bool) : (default=false) Does the engulfing candle require the wick to be engulfed as well?

Returns: A boolean - true if the current bar matches the requirements of a bearish engulfing candle

isInsideBar()

Detects inside bars

Returns: Returns true if the current bar is an inside bar

isOutsideBar()

Detects outside bars

Returns: Returns true if the current bar is an outside bar

barInSession(sess, useFilter)

Determines if the current price bar falls inside the specified session

Parameters:

sess (simple string) : The session to check

useFilter (bool) : (default=true) Whether or not to actually use this filter

Returns: A boolean - true if the current bar falls within the given time session

barOutSession(sess, useFilter)

Determines if the current price bar falls outside the specified session

Parameters:

sess (simple string) : The session to check

useFilter (bool) : (default=true) Whether or not to actually use this filter

Returns: A boolean - true if the current bar falls outside the given time session

dateFilter(startTime, endTime)

Determines if this bar's time falls within date filter range

Parameters:

startTime (int) : The UNIX date timestamp to begin searching from

endTime (int) : the UNIX date timestamp to stop searching from

Returns: A boolean - true if the current bar falls within the given dates

dayFilter(monday, tuesday, wednesday, thursday, friday, saturday, sunday)

Checks if the current bar's day is in the list of given days to analyze

Parameters:

monday (bool) : Should the script analyze this day? (true/false)

tuesday (bool) : Should the script analyze this day? (true/false)

wednesday (bool) : Should the script analyze this day? (true/false)

thursday (bool) : Should the script analyze this day? (true/false)

friday (bool) : Should the script analyze this day? (true/false)

saturday (bool) : Should the script analyze this day? (true/false)

sunday (bool) : Should the script analyze this day? (true/false)

Returns: A boolean - true if the current bar's day is one of the given days

atrFilter(atrValue, maxSize)

Parameters:

atrValue (float)

maxSize (float)

tradeCount()

Calculate total trade count

Returns: Total closed trade count

isLong()

Check if we're currently in a long trade

Returns: True if our position size is positive

isShort()

Check if we're currently in a short trade

Returns: True if our position size is negative

isFlat()

Check if we're currentlyflat

Returns: True if our position size is zero

wonTrade()

Check if this bar falls after a winning trade

Returns: True if we just won a trade

lostTrade()

Check if this bar falls after a losing trade

Returns: True if we just lost a trade

maxDrawdownRealized()

Gets the max drawdown based on closed trades (ie. realized P&L). The strategy tester displays max drawdown as open P&L (unrealized).

Returns: The max drawdown based on closed trades (ie. realized P&L). The strategy tester displays max drawdown as open P&L (unrealized).

totalPipReturn()

Gets the total amount of pips won/lost (as a whole number)

Returns: Total amount of pips won/lost (as a whole number)

longWinCount()

Count how many winning long trades we've had

Returns: Long win count

shortWinCount()

Count how many winning short trades we've had

Returns: Short win count

longLossCount()

Count how many losing long trades we've had

Returns: Long loss count

shortLossCount()

Count how many losing short trades we've had

Returns: Short loss count

breakEvenCount(allowanceTicks)

Count how many break-even trades we've had

Parameters:

allowanceTicks (float) : Optional - how many ticks to allow between entry & exit price (default 0)

Returns: Break-even count

longCount()

Count how many long trades we've taken

Returns: Long trade count

shortCount()

Count how many short trades we've taken

Returns: Short trade count

longWinPercent()

Calculate win rate of long trades

Returns: Long win rate (0-100)

shortWinPercent()

Calculate win rate of short trades

Returns: Short win rate (0-100)

breakEvenPercent(allowanceTicks)

Calculate break even rate of all trades

Parameters:

allowanceTicks (float) : Optional - how many ticks to allow between entry & exit price (default 0)

Returns: Break-even win rate (0-100)

averageRR()

Calculate average risk:reward

Returns: Average winning trade divided by average losing trade

unitsToLots(units)

(Forex) Convert the given unit count to lots (multiples of 100,000)

Parameters:

units (float) : The units to convert into lots

Returns: Units converted to nearest lot size (as float)

getFxPositionSize(balance, risk, stopLossPips, fxRate, lots)

(Forex) Calculate fixed-fractional position size based on given parameters

Parameters:

balance (float) : The account balance

risk (float) : The % risk (whole number)

stopLossPips (float) : Pip distance to base risk on

fxRate (float) : The conversion currency rate (more info below in library documentation)

lots (bool) : Whether or not to return the position size in lots rather than units (true by default)

Returns: Units/lots to enter into "qty=" parameter of strategy entry function

EXAMPLE USAGE:

string conversionCurrencyPair = (strategy.account_currency == syminfo.currency ? syminfo.tickerid : strategy.account_currency + syminfo.currency)

float fx_rate = request.security(conversionCurrencyPair, timeframe.period, close )

if (longCondition)

strategy.entry("Long", strategy.long, qty=zen.getFxPositionSize(strategy.equity, 1, stopLossPipsWholeNumber, fx_rate, true))

skipTradeMonteCarlo(chance, debug)

Checks to see if trade should be skipped to emulate rudimentary Monte Carlo simulation

Parameters:

chance (float) : The chance to skip a trade (0-1 or 0-100, function will normalize to 0-1)

debug (bool) : Whether or not to display a label informing of the trade skip

Returns: True if the trade is skipped, false if it's not skipped (idea being to include this function in entry condition validation checks)

fillCell(tableID, column, row, title, value, bgcolor, txtcolor, tooltip)

This updates the given table's cell with the given values

Parameters:

tableID (table) : The table ID to update

column (int) : The column to update

row (int) : The row to update

title (string) : The title of this cell

value (string) : The value of this cell

bgcolor (color) : The background color of this cell

txtcolor (color) : The text color of this cell

tooltip (string)

Returns: Nothing.

Systematic Investment PlanTradingview default strategy tester has few limitations. To name some:

Tradingview default strategy tester does not have option for periodic investment.

Does not allow reduce and refill kind of operations.

Comparison to buy and hold equity does not take into consideration on number of days invested

Hence, I created this as base for my further experiments with respect to strategies involving market timing.

Settings are quite simple and self explanatory.

Strategy NNFX Tester Strategy NNFX, Baseline, QQEs Fast C1, Slow C2, ATR, Volume and Exit

This is a Strategy Tester designed to work with Study (Alerts) of the same.

At time of creation based on Revision 8 of the Study.

DO NOT USE the Currency/Money Management section under settings. use the position sizing under "Inputs" - "Money Management" - "Risk per trade" which is defaulted to 2%

This has adjustable Baselines, Exits, ATR calculations, C1 and C2 are currently QQE & QQE Histo with adjustable settings but I'll include more choice of C1 & C2 as time goes on.

Find settings that work for you, then move them over to the Study version for best results.

Forward plans are to add much more options to both Alert/Strategy.

If anyone wants to collaborate or anything hit me up.

Parabolic SAR with Early Buy & MA-Based Exit Strategy📝 Strategy Description (Max SEO Impact)

This advanced Parabolic SAR-based trading strategy is designed to capture early trend reversals and exit intelligently using a dynamic moving average filter. It enters long trades when a PSAR reversal occurs, and exits only when the PSAR moves above price and the price falls below the 11-period SMA, helping avoid premature exits during volatile swings.

📌 Features:

• Custom Parabolic SAR calculation for refined trend tracking

• Background highlights during buy zones (SAR below price)

• Exit signals only when trend weakens (PSAR above + price under SMA)

• Red flag plotted on chart at exit bars for clear visual identification

• Works on all timeframes and instruments

Ideal for swing traders, trend followers, and strategy testers looking for smart PSAR-based entries with smoother exits.

Parabolic SAR with Early Buy & MA-Based Exit Strategy📝 Strategy Description (Max SEO Impact)